Following Hurricane Ian, the Florida legislature approved Senate Bill 2A in December 2022, emphasizing insurance affordability and accessibility within the state. A significant modification introduced by the bill is a novel stipulation requiring policyholders under the state-operated Citizens Property Insurance Corporation (Citizens) to carry flood insurance. Initially applicable to property owners in Special Flood Hazard Area (SFHA) zones, this requirement will eventually extend to encompass all Citizens-insured individuals.

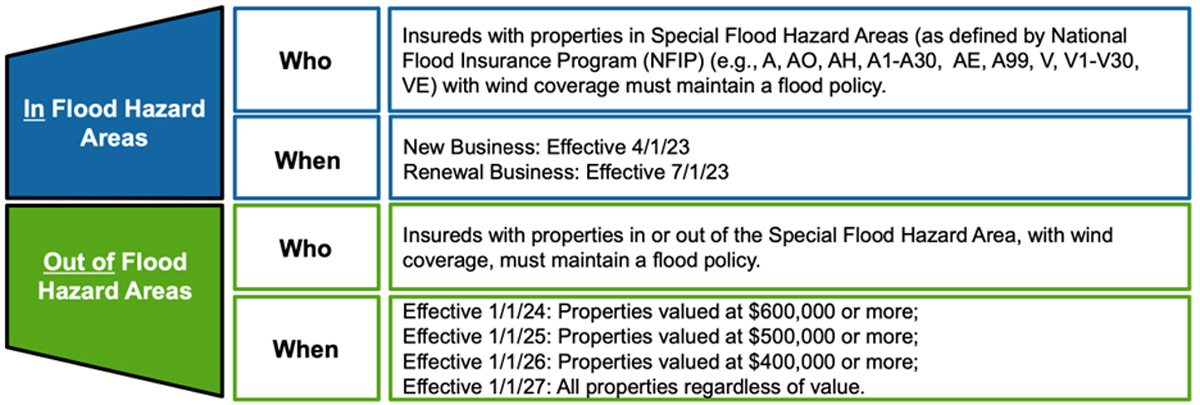

Commencing on April 1, 2023, for new policies and July 1, 2023, for renewals, the initial alteration affects residents in SFHA flood zones. Customers residing in these zones, previously carrying Wind coverage with Citizens, are now obligated to obtain flood insurance with corresponding dwelling and contents limits (or limits up to the NFIP maximum of $250k Dwelling and $100k Contents).

Citizens has initiated the issuance of non-renewal notices to all customers in SFHA flood zones with renewals scheduled on or after July 1, 2023. To rescind non-renewal, policyholders must submit a Flood Affirmation form along with proof of flood insurance.

For SFHA flood zone residents with Citizens homeowners insurance, compliance falls into three categories:

- Compliant: If you maintain matching building and contents limits on both your homeowners and flood policies or adhere to FEMA maximum limits of $250,000 dwelling and $100,000 contents, signing a Flood Affirmation form suffices.

- Non-Compliant: If you possess flood insurance but with inadequate coverage limits, adjustment and submission of a Flood Affirmation form are required. Alternatively, inadequate Contents limits can be rectified by removing coverage from Homeowners, though this is not recommended by agents.

- No Flood Insurance: Residents without flood insurance must purchase it to meet the requirements and sign the Flood Affirmation form. Flood insurance can be obtained through NFIP or private flood markets.

Will All Citizens Policyholders Be Required to Carry Flood Insurance?

The expanded flood requirements will eventually affect all Citizens policyholders, irrespective of their location in or outside SFHA flood zones (e.g., B, C, or X zones). Citizens will implement a phased approach, beginning with higher-value properties, outlined as follows:

- January 1, 2024: Properties with a replacement cost of $600k or more

- January 1, 2025: Properties with a replacement cost of $500k or more

- January 1, 2026: Properties with a replacement cost of $400k or more

- January 1, 2027: All properties, regardless of dwelling value

Citizens has devised a guide to simplify these new requirements:

Are Condo Unit Owners Impacted by Citizens’ New Flood Insurance Requirements?

Starting March 2023, condo unit owners are also mandated to adhere to these changes. However, Senate Bill 154, currently progressing through committees in Tallahassee, aims to eliminate the Flood insurance requirement for condo unit owners as long as the master condo association carries coverage. Our agents are closely monitoring the progress of this bill, recognizing its potential to alleviate the burden on many condo unit owners.

Insurance Resources Perspective on Citizens’ New Flood Insurance Requirements

Anticipating a substantial burden on numerous customers, we acknowledge our continuous advocacy for clients to maintain flood insurance regardless of their location. We understand that recent years have seen a significant increase in insurance costs due to factors such as abusive litigation, contractor fraud, inflation, and natural disasters like Hurricane Ian and Nicole. Additionally, the elevated costs of reinsurance (insurance for insurance companies) have contributed to the dramatic rise in flood insurance expenses for almost every customer in the Tampa Bay area, largely attributed to Risk Rating 2.0.

We foresee that many consumers may contemplate either discontinuing their insurance coverage entirely, dropping Wind coverage, or adjusting their contents to comply with the new guidelines. Consequently, we are skeptical about the potential benefits for consumers resulting from this new change.

At Insurance Resources, we collaborate with several private carriers that do not mandate Flood insurance. However, the reduction in the number of carriers within the state, with six going into receivership over the past year and others either leaving the state or tightening underwriting guidelines due to prolonged issues of abusive litigation and contractor fraud, has led to a significant increase in costs for the remaining private carriers. This has, in turn, prompted the migration of many policyholders to state-run Citizens.

What Can You Do If You Do Not Like the New Flood Insurance Requirements of Citizens?

We urge all consumers dissatisfied with these changes to reach out to their state representatives who endorsed the bill into law. Many legislators may not have considered the unforeseen ramifications and hardships these new requirements will impose on numerous Floridians.

For any inquiries about these recent changes, please feel free to contact one of our Florida agents at 866-400-7674.